Micro, Small, and Medium Enterprises (MSMEs) are crucial for economic development, and various governments often introduce schemes to support them. what is msme loan scheme? MSME loan schemes are initiatives aimed at providing financial assistance to these enterprises. These loans typically come with favorable terms such as lower interest rates and extended repayment periods to facilitate the growth and development of small businesses.

The specifics can vary by country and region, but the primary goal is to boost the MSME sector by addressing their financial needs. It’s a great way to encourage entrepreneurship and contribute to overall economic progress.

Who is eligible for MSME loan?

Eligibility criteria for MSME loans can vary depending on the country and the specific scheme. Some common factors that are often considered:

- Business Size: Typically, micro, small, and medium-sized enterprises are eligible. The specific criteria for each category may be based on factors such as investment in plant and machinery or equipment.

- Business Type: Different schemes might focus on specific sectors or types of businesses. Some schemes could be industry-specific or geared towards particular segments like women-owned enterprises or startups.

- Credit History: The financial health and credit history of the business and its owners may be evaluated to determine eligibility.

- Legal Structure: The legal structure of the business may also be a factor. Sole proprietorships, partnerships, and private limited companies may have different criteria.

- Operational History: Some schemes may require a minimum operational history for the business, ensuring a certain level of stability and experience.

- Compliance with Regulatory Requirements: Meeting regulatory requirements and compliance with local laws and regulations is often a prerequisite.

- Purpose of the Loan: The intended use of the loan may be considered. For example, some schemes might be designed for working capital, while others may focus on expansion or technology adoption.

It’s essential for potential applicants to check the specific eligibility criteria of the MSME loan scheme they are interested in, as these can vary widely. Local financial institutions or government agencies administering the scheme usually provide detailed information on eligibility requirements.

What are the Benefits of MSME loan?

MSME loans offer several benefits to small and medium-sized enterprises, contributing to their growth and development. Here are some common benefits associated with MSME loans:

- Financial Support: MSME loans provide much-needed financial assistance to businesses that may face challenges in raising capital through other means.

- Low Interest Rates: Many MSME loan schemes come with lower interest rates compared to traditional loans, making it more affordable for small businesses to borrow and invest in their operations.

- Flexible Repayment Terms: These loans often come with flexible repayment terms, allowing businesses to choose a repayment schedule that aligns with their cash flow and revenue cycles.

- Collateral Requirements: Some MSME loan schemes may have relaxed collateral requirements, making it easier for businesses with limited assets to qualify for the loan.

- Technology Adoption: Certain MSME loan programs may specifically target technology adoption and innovation, helping businesses modernize and stay competitive in the market.

- Job Creation: By providing financial support to MSMEs, these loans contribute to job creation, fostering economic development and stability.

- Skill Enhancement: Some schemes may include components for skill development and training, empowering entrepreneurs and employees with the necessary skills to enhance productivity.

- Government Incentives: Governments often provide incentives and subsidies as part of MSME loan schemes, reducing the overall financial burden on businesses.

- Promotion of Entrepreneurship: MSME loans encourage entrepreneurship by providing aspiring business owners with the financial means to start and sustain their ventures.

- Economic Growth: The overall impact of MSME loans is positive for the economy, as these businesses contribute significantly to employment, production, and innovation.

It’s important for businesses to carefully review the terms and conditions of specific MSME loan schemes to understand the full range of benefits available to them.

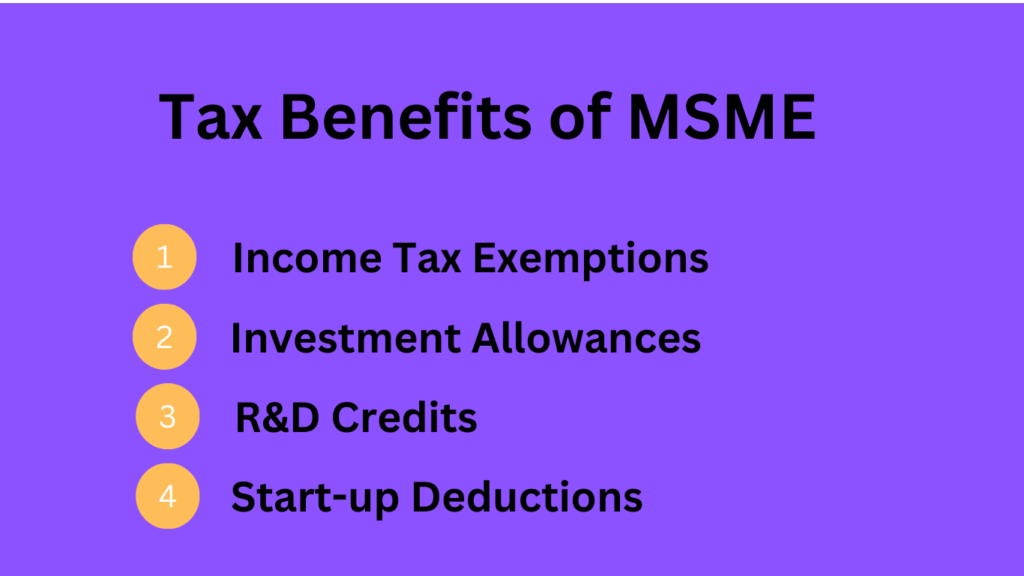

What are the Tax Benefits of MSME?

Tax benefits for Micro, Small, and Medium Enterprises (MSMEs) can vary by country and region. However, there are some common tax incentives and benefits that many governments offer to support the growth of MSMEs. Here are a few examples:

- Income Tax Exemptions: Some countries provide income tax exemptions or reduced tax rates for MSMEs to ease their financial burden and encourage business growth.

- Investment Allowances: Governments may offer investment allowances, allowing MSMEs to deduct a certain percentage of their investment in machinery, equipment, or infrastructure from their taxable income.

- R&D Credits: Tax credits for research and development (R&D) activities are often available to encourage MSMEs to invest in innovation and technology.

- Start-up Deductions: Start-ups and small businesses may qualify for special deductions or exemptions during their initial years of operation to help them establish themselves in the market.

- Goods and Services Tax (GST) Relief: Some countries provide relief or exemptions on Goods and Services Tax for MSMEs, reducing the overall indirect tax burden on their products and services.

- Customs Duty Benefits: Incentives such as customs duty exemptions or reductions on the import of certain raw materials or equipment may be offered to MSMEs.

- Employment-Related Incentives: Governments may introduce incentives related to employment, such as deductions for the creation of new jobs or training programs for employees.

- Carry Forward of Losses: MSMEs may be allowed to carry forward losses incurred in one financial year to offset against future profits, providing them with tax relief in subsequent years.

- Compliance Relaxations: Governments may simplify compliance procedures for MSMEs, reducing the administrative burden and compliance costs associated with tax filings.

It’s important for MSMEs to stay informed about the specific tax regulations and incentives in their respective regions, as they can have a significant impact on the overall financial health of the business. Consulting with a tax professional or financial advisor is advisable to ensure that businesses take full advantage of available tax benefits.

How to Apply for MSME loan from government?

Applying for an MSME loan from the government typically involves a structured process.

- Research and Identify Schemes: Research and identify the specific MSME loan schemes offered by the government. Different schemes may cater to different business needs and sectors.

- Check Eligibility Criteria: Review the eligibility criteria for the chosen scheme. Ensure that your business meets the necessary requirements regarding size, sector, credit history, and other relevant factors.

- Prepare Necessary Documents: Gather and prepare all the required documents. This may include business registration documents, financial statements, business plan, project report, and any other documents specified by the lending institution.

- Visit the Relevant Government Portal: Many governments provide online portals for loan applications. Visit the official government website or the website of the relevant financial institution overseeing the MSME loan scheme.

- Create an Account: If required, create an account on the portal to initiate the application process. Provide accurate and up-to-date information about your business.

- Fill Out the Application Form: Complete the application form with the necessary details. Verify that the details furnished are precise and align with the accompanying documents.

- Attach Supporting Documents: Upload or submit all the required supporting documents as per the instructions provided in the application form. Make sure the documents are organized and easy to verify.

- Submit the Application: Submit the completed application form along with the supporting documents through the online portal or the designated application channel. Some schemes may also allow for physical submission of documents.

- Application Review: The government or the financial institution will review your application. This process may take some time, and they may request additional information or clarification if needed.

- Approval and Disbursement: If your application is approved, you will receive notification, and the funds will be disbursed according to the terms of the loan agreement. Be sure to understand the terms and conditions before accepting the loan.

- Monitor Compliance: After receiving the loan, ensure compliance with any reporting requirements or conditions specified by the lending institution. This may include periodic financial reporting or updates on the progress of your business.

It’s advisable to seek assistance from local MSME support agencies or financial advisors to navigate the application process effectively. They can provide guidance on specific requirements and help ensure that your application is complete and well-prepared.

How much loan can I get from MSME?

The amount of loan you can get from MSME schemes varies widely and depends on several factors. Here are some key considerations that can influence the loan amount:

- Scheme and Government Policies: Different MSME loan schemes may have different maximum loan limits based on the government’s policies and objectives. Check the specific details of the scheme you are applying for.

- Business Size and Type: The loan amount may be influenced by the size and type of your business. Micro, small, and medium enterprises may have different maximum loan limits.

- Financial Health: The financial health of your business, as indicated by factors such as revenue, profitability, and creditworthiness, can influence the loan amount. Lenders might evaluate your capacity to settle the loan.

- Purpose of the Loan: The intended use of the loan can also impact the amount you can borrow. For example, loans for working capital needs might have different limits than those for capital expenditure or technology adoption.

- Collateral and Security: The availability and value of collateral or security you can provide may affect the loan amount. Some MSME loan schemes may have relaxed collateral requirements, while others may require specific assets as security.

- Credit History: Your credit history and repayment track record can be a crucial factor in determining the loan amount. A positive credit history may increase your eligibility for a higher loan amount.

- Market Conditions: Economic conditions and market trends can also play a role. In certain situations, governments may adjust loan limits or introduce special provisions based on economic factors.

To determine the specific loan amount you can get from an MSME scheme, it’s essential to review the guidelines and criteria outlined by the relevant government agency or financial institution administering the scheme. Additionally, consider consulting with a financial advisor or reaching out to local MSME support organizations for personalized guidance based on your business’s unique circumstances.

What is MSME loan interest rate?

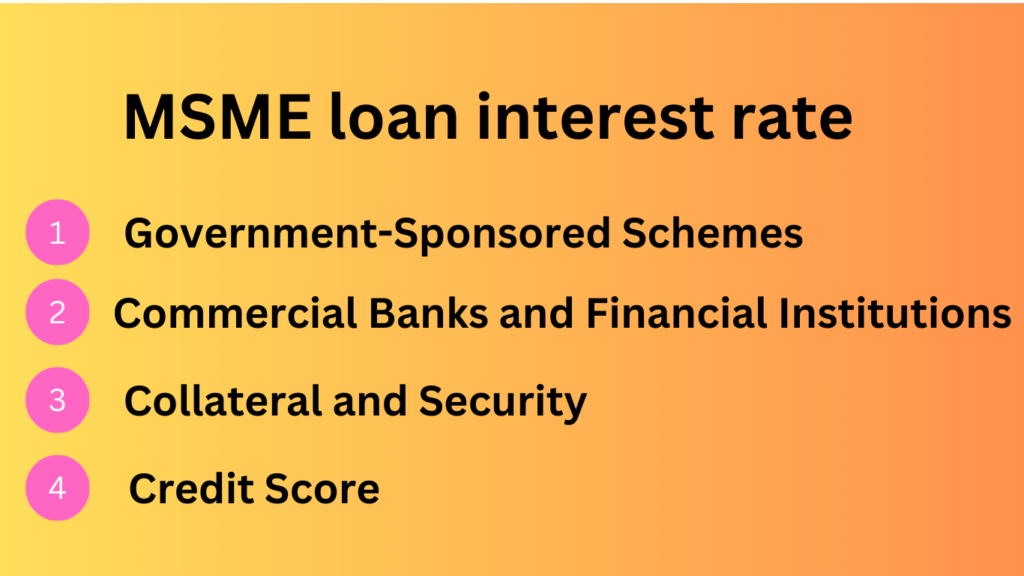

The interest rates for MSME loans can vary based on several factors, including the lending institution, the specific MSME loan scheme, the borrower’s creditworthiness, and prevailing market conditions. I can provide you with a general idea of the range of interest rates for MSME loans.

- Government-Sponsored Schemes: In many countries, government-sponsored MSME loan schemes may offer subsidized or lower interest rates to encourage the growth of small and medium-sized enterprises. These rates can be more favorable compared to standard commercial loans.

- Commercial Banks and Financial Institutions: Commercial banks and financial institutions also provide MSME loans, and the interest rates may vary. Rates are often influenced by factors such as the borrower’s credit profile, the purpose of the loan, and the overall risk associated with the loan.

- Collateral and Security: The availability and value of collateral or security offered by the borrower can impact the interest rate. Loans with collateral may have lower interest rates compared to unsecured loans.

- Credit Score: The creditworthiness of the borrower, as indicated by their credit score, can influence the interest rate. Businesses with a strong credit history may qualify for lower interest rates.

- Market Conditions: Overall economic conditions and market trends can affect interest rates. During periods of economic stability, interest rates may be more competitive.

To obtain the most accurate and up-to-date information on MSME loan interest rates, it’s recommended to check with the specific lending institution offering the loan or visit their official website. Additionally, consider consulting with a financial advisor who can provide guidance based on your business’s unique circumstances and help you navigate the loan application process effectively.

MSME loan interest rate subsidy

MSME loan interest rate subsidies are often provided by governments as a means of supporting the growth and development of Micro, Small, and Medium Enterprises (MSMEs). These subsidies aim to make borrowing more affordable for small businesses and encourage entrepreneurship. The specifics of interest rate subsidies can vary by country and region, and they are often part of government-sponsored MSME loan schemes.

In India, government initiatives provide numerous benefits for MSMEs, ranging from collateral-free loans and accessible credit facilities to favorable tax conditions, improved interest rates, and subsidies for MSME loans. To avail themselves of these support measures, MSMEs need to register with the government and obtain an MSME or Udyam Certificate.

Additionally, both public sector and private banks in India offer MSME Loans through various government programs. The government regularly introduces measures to facilitate the growth of small businesses and provide them with essential support. Several active MSME loan schemes include popular ones like Mudra Loans, Credit Guarantee Trust Fund for Micro and Small Enterprises (CGTMSE), and the Prime Minister’s Employment Generation Programme (PMEGP).

For example, the Mudra Loan scheme aims to ensure sufficient credit facilities for small businesses, particularly focusing on priority sector lending. The CGTMSE scheme provides collateral-free loans (up to Rs 1 crore) to both new and existing micro and small industries.

The government has also introduced the Interest Subvention Scheme for MSMEs, where both scheduled commercial and co-operative banks are eligible lending institutions. Under this MSME loan subsidy scheme, eligible firms can benefit from a two percent per annum interest relief on their outstanding fresh/incremental term loans or working capital loans during the scheme’s active period. The scheme covers all term loans and working capital loans to MSMEs, up to a limit of Rs 1 crore (Rs 100 lakh). However, to qualify for relief under this MSME loan subsidy scheme, the loan amount should not have been declared a Non-Performing Asset (NPA) at the time of filing the claim.

Key points regarding MSME loan interest rate subsidies:

- Government-Sponsored Schemes: Many governments introduce schemes specifically designed for MSMEs, offering subsidized interest rates as an incentive for businesses to access financing.

- Reduced Interest Costs: Interest rate subsidies effectively reduce the cost of borrowing for MSMEs, making it more feasible for them to invest in operations, expansion, or technology adoption.

- Targeted Sectors and Categories: Some interest rate subsidy programs may be targeted at specific sectors or categories of MSMEs, such as women-owned enterprises, startups, or those engaged in certain industries.

- Qualification Criteria: MSMEs looking to benefit from interest rate subsidies typically need to meet specific eligibility criteria outlined by the government or relevant financial institutions. Criteria may include factors like business size, credit history, and compliance with regulations.

- Collateral and Security: Depending on the scheme, there may be relaxed collateral requirements or alternative arrangements to facilitate access to subsidized interest rates.

- Application Process: MSMEs interested in availing the interest rate subsidy should follow the application process outlined by the government or the administering financial institution. This usually involves submitting necessary documents and meeting specified requirements.

- Monitoring and Compliance: Businesses that receive interest rate subsidies may be required to comply with certain conditions, such as reporting on the use of funds or meeting specific business development targets.

To access specific details about MSME loan interest rate subsidies, it’s crucial to check with the relevant government agencies, financial institutions, or official websites for the most up-to-date and accurate information. Consulting with local business associations or seeking guidance from financial advisors can also provide valuable insights into available subsidy programs.

What is 15 lakh subsidy for MSME?

Subsidies and government support programs can vary by country and region, and they often undergo changes over time.

If there have been updates or new schemes introduced since then, it’s essential to check the latest information from the relevant government authorities or financial institutions in your specific region. MSME subsidies and support programs are typically designed to promote the growth and development of Micro, Small, and Medium Enterprises, and they may cover various aspects such as access to credit, technology adoption, skill development, and more.

To get accurate and up-to-date details about any 15 lakh subsidy or related support for MSMEs, consider the following steps:

- Check Government Announcements: Look for recent announcements or updates from the government regarding MSME subsidies. Government websites and official press releases are good sources for this information.

- Visit Official MSME Portals: Many countries have dedicated portals or departments specifically for MSMEs. Check these official platforms for the latest information on available subsidies and support.

- Contact Local MSME Support Agencies: Reach out to local MSME support agencies, business development centers, or chambers of commerce. They may have information on the latest government initiatives and subsidies.

- Consult with Financial Institutions: Financial institutions, including banks and credit agencies, may be aware of the latest subsidy programs for MSMEs. Inquire with them about any subsidies available for businesses.

- Professional Advice: Consider seeking advice from financial advisors or consultants who specialize in MSMEs. They can provide insights into available subsidies and guide you through the application process.

Remember that government programs and subsidies are subject to change, and staying informed about the latest developments is crucial for businesses looking to benefit from such initiatives.

Read more:

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.